")

")

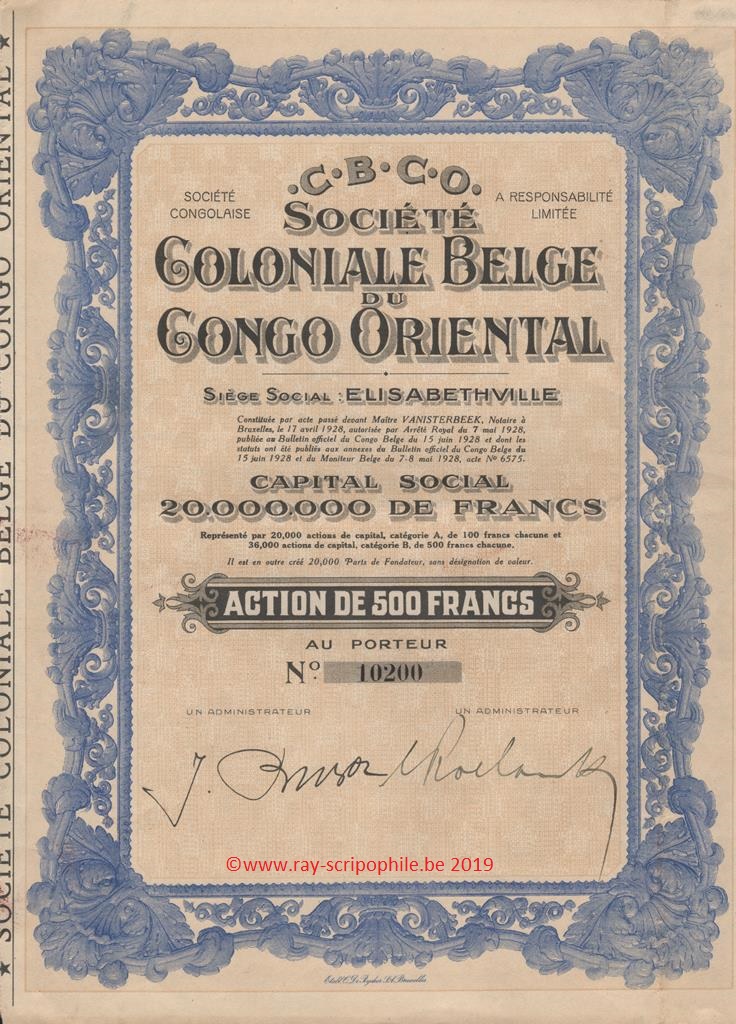

C.B.C.O. - SOCIETE COLONIALE BELGE DU CONGO ORIENTAL S.C.R.L.

Constitution

The Société Coloniale Belge du Congo Oriental (C. B. C. O.) S.C.R.L. was incorporated on April 17, 1928. The head office was established in Elisabethville, the administrative office in Brussels.

The share capital was fixed at twenty million francs, represented by 20,000 class A shares of 100 francs and 36,000 class B shares of 500 francs. 20,000 founder's shares were created without any value designation.

The capital shares were subscribed for in cash by the respondents : List

All shares were paid up by 20% and the sum of four million francs was made available to the new company (30 - (1928) 909 to 928).

Contributions(s)

Mr. Jean-Pierre Buzon contributed to the presently constituted company, which was accepted by the other participants, of the benefit of his work, steps, and studies in view of the constitution of the present company.

In remuneration of this contribution, Mr. Jean-Pierre Buzon was allotted the 20,000 founder's shares (30 - (1928) 909 to 928).

First board of directors

The first assembly fixed the number of members to compose the first board of directors at ten and appointed to these functions of directors, Messrs.:

Benoit Gravez, Louis Chaltin, Jean-Pierre Buzon, Louis Roelants, Maurice Desclée, Emilien Auger, Charles Marc, Marcel Loumaye, Gustave Jonas and General E. Henry.

Fixed at four the number of members to compose the first college of commissioners and called to the functions of commissioners, Messrs.:

Charles Coene, Adolphe Lépreux, Mrs. Marie Buntinx, Raymond De Nucé (30 - (1928) 909 to 928).

Object

To conduct all commercial, industrial, agricultural, forestry, mining, real estate, financial and other operations in the Belgian Congo and particularly in Katanga and the neighboring regions.

To be able to acquire, sell, rent or lease all properties or concessions, to exploit directly or indirectly the products of the soil and the subsoil, whatever they are, to transform them, to manufacture the articles which are related to its trade or its industry, to take an interest in all industries or operations whose object is similar or related to its own or could be useful for its realization, to form special associations or companies for any of these enterprises or to participate in other associations or companies or in their operations by any means (30 - (1928) 909 to 928).

Modification of the capital, évent(s), participation(s), dividende(s), quotation

A subsidiary of the Société Mutuelle Belgo-Coloniale, the C.B.C.O. decided to establish itself in Elisabethville and Likasi-Panda with the intention of opening department stores. In 1928, it acquired two properties in the center of Elisabethville. It also set up in Port-Francqui in the buildings of the sister company Comptoir Belge-Congolais de Matériaux (Belcoma). It conducted commercial operations there on a regular basis since December 1928. In Elisabethville, the Company only started commercial operations in March 1929.

Despite the commercial crisis which had been raging in Katanga since the end of 1928, a crisis which caused the realization of important stocks of goods, the sales progressed continuously. It also succeeded in Port-Francqui (21 - (1930 T1) 590/91).

Fiscal year 1929-30 - The major installation at Elisabethville was well on the way to completion, and at Likasi the foundations of the building were completed. The commercial crisis was still raging in Katanga, as in the rest of the colony, but there were indications that the problem would not get worse. Operations were slowed down because of the crisis, but nevertheless allowed the company to present a favorable balance sheet.

The 1930-31 fiscal year. - The Company was affected by the crisis that hit the Colony; the fiscal year ended in a loss. Since July 1931, severe cost-cutting measures have been taken. The result of these measures will only be seen in the accounts for the current fiscal year ending June 30, 1932. The Company's commercial activity in Kasai and Katanga was reduced to the extent that the large industrial organizations in these regions had to reduce their own activity. The construction of the building in Elisabethville was continued, but slowly. While waiting for better times, the Company stopped its construction work in Jadotville.

The 1931-32 fiscal year - The results reflected the tricky situation in which trade in the Katanga and Kasai regions is struggling. A new economic upswing can only come from a recovery of the copper market. The deficit which, as of June 30, 1931, amounted to 1,198,647.26 francs was increased by 2,918,987.68 francs for the current fiscal year, making a total deficit of 4,117,634.94 francs (21 - (1933 T1) - 999).

Until the reduction of the capital in 1935, the Company only made losses, and at the end of 1934 had a deficit balance of 10,442,400.07 francs (30 - (1935) - 48).

On June 11, 1935, the EGM decided to transform the 20,000 A shares into B shares, the transformation was done at the rate of one B share for five A shares (suppression of the categories) and to reduce the capital by 15 million to 5 million by reducing the nominal value to 125 francs for the 40,000 merged shares (30 - (1935) - 513).

From the time of the reduction of the capital, the results of the Company were positive.

Merger

On November 15, 1939, the EGM of the Mutuelle Belgo-Coloniale decided to absorb, by way of merger, the Congolese company C.B.C.O. "Société Coloniale Belge du Congo Oriental". For this operation, the capital of the Mutuelle Belgo-Coloniale was increased by 2,150 million francs by the creation and issue of 17,200 new fully paid-up shares which were attributed to the company C.B.C.O. in remuneration of the assets and liabilities. The C.B.C.O. shares belonging to the Société Mutuelle Belgo-Coloniale were cancelled (23,034 capital shares and 14,150 founder's shares) (12 - (24/01/1940)-624).